40. Optimal Unemployment Insurance#

40.1. Overview#

This lecture describes a model of optimal unemployment insurance created by Shavell and Weiss (1979) [Shavell and Weiss, 1979].

We use recursive techniques of Hopenhayn and Nicolini (1997) [Hopenhayn and Nicolini, 1997] to compute optimal insurance plans for Shavell and Weiss’s model.

Hopenhayn and Nicolini’s model is a generalization of Shavell and Weiss’s along dimensions that we’ll soon describe.

40.2. Shavell and Weiss’s Model#

An unemployed worker orders stochastic processes of

consumption and search effort

where

We assume that

We require that

All jobs are alike and pay wage

An unemployed

worker searches with effort

Furthermore,

The probability

of finding a job is

Note

When we compute examples below, we’ll use assume the same

The consumption good is nonstorable.

An unemployed worker has no savings and cannot borrow or lend.

The unemployed worker’s only source of consumption smoothing over time and across states is an insurance agency or planner.

Once a worker has found a job, he is beyond the planner’s grasp.

This is Shavell and Weiss’s assumption, but not Hopenhayn and Nicolini’s.

Hopenhayn and Nicolini allow the unemployment insurance agency to impose history-dependent taxes on previously unemployed workers.

Since there is no incentive problem after the worker has found a job, it is optimal for the agency to provide an employed worker with a constant level of consumption.

Hence, Hopenhayn and Nicolini’s insurance agency imposes a permanent per-period history-dependent tax on a previously unemployed but presently employed worker.

40.2.1. Autarky#

As a benchmark, we first study the fate of an unemployed worker who has no access to unemployment insurance.

Because employment is an absorbing state for the worker, we work backward from that state.

Let

Once the worker is employed,

Therefore,

Now let

Value

The first-order condition for a maximum is

with equality if

Since there is no state variable in this

infinite horizon problem, there is a time-invariant optimal

search intensity

Let

Equations (40.3)

and (40.4)

form the basis for

an iterative algorithm for computing

40.2.2. Full Information#

Another benchmark model helps set the stage for the model with private information that we ultimately want to study.

We temporarily assume that an unemployment insurance agency has full information about the unemployed worker.

We assume that the insurance agency can control both the consumption and the search effort of an unemployed worker.

The agency wants to design an unemployment insurance contract to give

the unemployed worker expected discounted utility

The agency, i.e., the planner, wants to deliver value

We formulate the optimal insurance problem recursively.

Let

The cost function is strictly convex because

a higher

Given

The planner sets

where minimization is subject to the promise-keeping constraint

Here

The right side of Bellman equation (40.5) is attained by

policy functions

The promise-keeping constraint,

equation (40.6),

asserts that the 3-tuple

Let

At an interior solution, first-order

conditions with

respect to

The envelope condition

Strict convexity of

Applied repeatedly over time,

The first equation of (40.7)

determines

That

Thus, the unemployed worker’s consumption

But the worker’s consumption is not smoothed across states of

employment and unemployment unless

40.2.3. Incentive Problem#

The preceding efficient insurance scheme assumes that the insurance agency

controls both

The insurance agency cannot simply provide

Here is why.

The agency delivers a value

It increases the unemployed worker’s consumption

The prescribed

search effort is higher than what the worker would choose

if he were to be guaranteed consumption level

This follows from the first two equations of (40.7) and the

fact that the insurance scheme is costly,

Now look at the worker’s first-order condition (40.4) under autarky.

It implies that if search effort

If he were free to choose

Starting from the

If an equality can be established before

Thus, since the worker does not take the cost of the insurance scheme into account, he would choose a search effort below the socially optimal, full-information level.

The full-information contract thus relies on the agency’s ability to control both the unemployed worker’s consumption and his search effort.

40.3. Private Information#

Following [Shavell and Weiss, 1979] and

[Hopenhayn and Nicolini, 1997], now assume that the unemployment insurance agency cannot

observe or control

The worker is free to choose

We are assuming that the worker’s best response to the unemployment insurance arrangement is completely characterized by the first-order condition (40.4), an instance of the so-called first-order approach to incentive problems.

Given a contract, the individual will choose search effort according to first-order condition (40.4).

This fact motivates the insurance agency to design an unemployment insurance contract that respects this restriction.

Thus, the contract design problem is now to minimize the right side of equation (40.5) subject to expression (40.6) and the incentive constraint (40.4).

Since the restrictions (40.4) and (40.6) are not linear

and generally do not define a convex set, it becomes challenging

to provide conditions under which the solution to the dynamic

programming problem results in a convex function

Sometimes this complication can be handled by convexifying the constraint set by introducing lotteries.

A common finding is that optimal plans do not involve lotteries, because convexity of the constraint set is a sufficient but not necessary condition for convexity of the cost function.

In order to characterize the optimal solution, we follow Hopenhayn and Nicolini (1997) [Hopenhayn and Nicolini, 1997] by hopefully proceeding under the assumption that

Let

But now we replace the weak inequality in (40.6) by an equality.

We do this because the unemployment insurance agency cannot award a higher utility than

At an interior solution, first-order conditions with

respect to

where the second equality in the second equation in (40.8) follows from strict equality

of the incentive constraint (40.4) when

As long as the

insurance scheme is associated with costs, so that

The first-order condition in the second equation of the third equality in (40.8) and the

envelope condition

Convexity of

After we have also used the first equation of (40.8), it follows that in order to provide the proper incentives, the consumption of the unemployed worker must decrease as the duration of the unemployment spell lengthens.

It also follows from (40.4) at equality that

search effort

The of benefits on the duration of unemployment is designed to provide the worker an incentive to search.

To understand this, from the third equation of (40.8), notice how

the conclusion that consumption falls with the duration of

unemployment depends on the assumption that more search effort

raises the prospect of finding a job, i.e., that

If

Thus, when

40.3.1. Computational Details#

It is useful to note that there

are natural lower and upper bounds to the set

of continuation values

The lower bound is

the expected lifetime utility in autarky,

To compute an upper bound, represent condition (40.4) as

with equality if

If there is zero search effort, then

Therefore, to rule out zero search effort we require

(Remember that

This step gives our upper bound

for

To formulate the Bellman equation numerically,

we suggest using the constraints to eliminate

First express the promise-keeping constraint (40.6) at equality as

so that consumption is

Similarly, solving the inequality (40.4) for

When we specialize (40.10) to the functional

form for

Formulas (40.9) and (40.11) express

Using these functions

allows us to write the Bellman equation in

40.3.2. Python Computations#

We’ll approximate the planner’s optimal cost function with cubic splines.

To do this, we’ll load some useful modules

import numpy as np

import scipy as sp

import matplotlib.pyplot as plt

We first create a class to set up a particular parametrization.

class params_instance:

def __init__(self,

r,

β = 0.999,

σ = 0.500,

w = 100,

n_grid = 50):

self.β,self.σ,self.w,self.r = β,σ,w,r

self.n_grid = n_grid

uw = self.w**(1-self.σ)/(1-self.σ) #Utility from consuming all wage

self.Ve = uw/(1-β)

40.3.3. Parameter Values#

For the other parameters appearing in the above Python code, we’ll calibrate parameter

In particular, we seek an p(a(r)) = 0.1, where a is the optimal search effort.

First, we create some helper functions.

# The probability of finding a job given search effort, a and parameter r.

def p(a,r):

return 1-np.exp(-r*a)

def invp_prime(x,r):

return -np.log(x/r)/r

def p_prime(a,r):

return r*np.exp(-r*a)

# The utiliy function

def u(self,c):

return (c**(1-self.σ))/(1-self.σ)

def u_inv(self,x):

return ((1-self.σ)*x)**(1/(1-self.σ))

Recall that under autarky the value for an unemployed worker satisfies the Bellman equation

At the optimal choice of

with equality when a >0.

Given a value of parameter

Guess

Given

Evaluate the difference between the LHS and RHS of the Bellman equation (40.13)

Update guess for

For a given Vu_error calculates the error in the Bellman equation under the optimal search intensity.

We’ll soon use this as an input to computing

# The error in the Bellman equation that requires equality at

# the optimal choices.

def Vu_error(self,Vu,r):

β= self.β

Ve = self.Ve

a = invp_prime(1/(β*(Ve-Vu)),r)

error = u(self,0) -a + β*(p(a,r)*Ve + (1-p(a,r))*Vu) - Vu

return error

Since the calibration exercise is to match the hazard rate under autarky to the data, we must find a parameter p(a,r) = 0.1.

The function below r_error calculates, for a given guess of

We’ll use this to compute a calibrated

# The error of our p(a^*) relative to our calibration target

def r_error(self,r):

β = self.β

Ve = self.Ve

Vu_star = sp.optimize.fsolve(Vu_error_Λ,15000,args = (r))

a_star = invp_prime(1/(β*(Ve-Vu_star)),r) # Assuming a>0

return p(a_star,r) - 0.1

Now, let us create an instance of the model with our parametrization

params = params_instance(r = 1e-2)

# Create some lambda functions useful for fsolve function

Vu_error_Λ = lambda Vu,r: Vu_error(params,Vu,r)

r_error_Λ = lambda r: r_error(params,r)

We want to compute an

To do so, we will use a bisection strategy.

r_calibrated = sp.optimize.brentq(r_error_Λ,1e-10,1-1e-10)

print(f"Parameter to match 0.1 hazard rate: r = {r_calibrated}")

Vu_aut = sp.optimize.fsolve(Vu_error_Λ,15000,args = (r_calibrated))[0]

a_aut = invp_prime(1/(params.β*(params.Ve-Vu_aut)),r_calibrated)

print(f"Check p at r: {p(a_aut,r_calibrated)}")

Parameter to match 0.1 hazard rate: r = 0.0003431409393866592

Check p at r: 0.10000000000001996

/tmp/ipykernel_9649/2412693371.py:6: RuntimeWarning: The iteration is not making good progress, as measured by the

improvement from the last five Jacobian evaluations.

Vu_star = sp.optimize.fsolve(Vu_error_Λ,15000,args = (r))

Now that we have calibrated our the parameter

40.3.4. Computation under Private Information#

Our approach to solving the full model follows ideas of Judd (1998) [Judd, 1998], who uses a polynomial to approximate the value function and a numerical optimizer to perform the optimization at each iteration.

Note

For further details of the Judd (1998) [Judd, 1998] method, see [Ljungqvist and Sargent, 2018], Section 5.7.

We will use cubic splines to interpolate across a pre-set grid of points to approximate the value function.

Our strategy involves finding a function

Notice that in equations (40.9) and (40.11), we have analytical solutions of

We can substitute these equations for

def calc_c(self,Vu,V,a):

'''

Calculates the optimal consumption choice coming from the constraint of the insurer's problem

(which is also a Bellman equation)

'''

β,Ve,r = self.β,self.Ve,self.r

c = u_inv(self,V + a - β*(p(a,r)*Ve + (1-p(a,r))*Vu))

return c

def calc_a(self,Vu):

'''

Calculates the optimal effort choice coming from the worker's effort optimality condition.

'''

r,β,Ve = self.r,self.β,self.Ve

a_temp = np.log(r*β*(Ve - Vu))/r

a = max(0,a_temp)

return a

With these analytical solutions for optimal

With this in hand, we have our algorithm.

40.3.5. Algorithm#

Fix a set of grid points

Guess a function

For each point in

Evaluating the minimum across all points in

If

Thus, the iterations are

The function iterate_C below executes step 3 in the above algorithm.

# Operator iterate_C that calculates the next iteration of the cost function.

def iterate_C(self,C_old,Vu_grid):

'''

We solve the model by minimising the value function across a grid of possible promised values.

'''

β,r,n_grid = self.β,self.r,self.n_grid

C_new = np.zeros(n_grid)

cons_star = np.zeros(n_grid)

a_star = np.zeros(n_grid)

V_star = np.zeros(n_grid)

C_new2 = np.zeros(n_grid)

V_star2 = np.zeros(n_grid)

for V_i in range(n_grid):

C_Vi_temp = np.zeros(n_grid)

cons_Vi_temp = np.zeros(n_grid)

a_Vi_temp = np.zeros(n_grid)

for Vu_i in range(n_grid):

a_i = calc_a(self,Vu_grid[Vu_i])

c_i = calc_c(self,Vu_grid[Vu_i],Vu_grid[V_i],a_i)

C_Vi_temp[Vu_i] = c_i + β*(1-p(a_i,r))*C_old[Vu_i]

cons_Vi_temp[Vu_i] = c_i

a_Vi_temp[Vu_i] = a_i

# Interpolate across the grid to get better approximation of the minimum

C_Vi_temp_interp = sp.interpolate.interp1d(Vu_grid,C_Vi_temp, kind = 'cubic')

cons_Vi_temp_interp = sp.interpolate.interp1d(Vu_grid,cons_Vi_temp, kind = 'cubic')

a_Vi_temp_interp = sp.interpolate.interp1d(Vu_grid,a_Vi_temp, kind = 'cubic')

res = sp.optimize.minimize_scalar(C_Vi_temp_interp,method='bounded',bounds = (Vu_min,Vu_max))

V_star[V_i] = res.x

C_new[V_i] = res.fun

# Save the associated consumpton and search policy functions as well

cons_star[V_i] = cons_Vi_temp_interp(V_star[V_i])

a_star[V_i] = a_Vi_temp_interp(V_star[V_i])

return C_new,V_star,cons_star,a_star

The following code executes steps 4 and 5 in the Algorithm until convergence to a function

def solve_incomplete_info_model(self,Vu_grid,Vu_aut,tol = 1e-6,max_iter = 10000):

iter = 0

error = 1

C_init = np.ones(self.n_grid)*0

C_old = np.copy(C_init)

while iter<max_iter and error >tol:

C_new,V_new,cons_star,a_star = iterate_C(self,C_old,Vu_grid)

error = np.max(np.abs(C_new - C_old))

#Only print the iterations every 50 steps

if iter % 50 ==0:

print(f"Iteration: {iter}, error:{error}")

C_old = np.copy(C_new)

iter+=1

return C_new,V_new,cons_star,a_star

40.4. Outcomes#

Using the above functions, we create another instance of the parameters with our calibrated parameter

##? Create another instance with the correct r now

params = params_instance(r = r_calibrated)

#Set up grid

Vu_min = Vu_aut

Vu_max = params.Ve - 1/(params.β*p_prime(0,params.r))

Vu_grid = np.linspace(Vu_min,Vu_max,params.n_grid)

#Solve model

C_star,V_star,cons_star,a_star = solve_incomplete_info_model(params,Vu_grid,Vu_aut,tol = 1e-6,max_iter = 10000) #,cons_star,a_star

# Since we have the policy functions in grid form, we will interpolate them to be able to

# evaluate any promised value

cons_star_interp = sp.interpolate.interp1d(Vu_grid,cons_star)

a_star_interp = sp.interpolate.interp1d(Vu_grid,a_star)

V_star_interp = sp.interpolate.interp1d(Vu_grid,V_star)

Iteration: 0, error:72.95964854907824

Iteration: 50, error:12.222761762480786

Iteration: 100, error:0.12875960366727668

Iteration: 150, error:0.0009402349710398994

Iteration: 200, error:6.115462838351959e-06

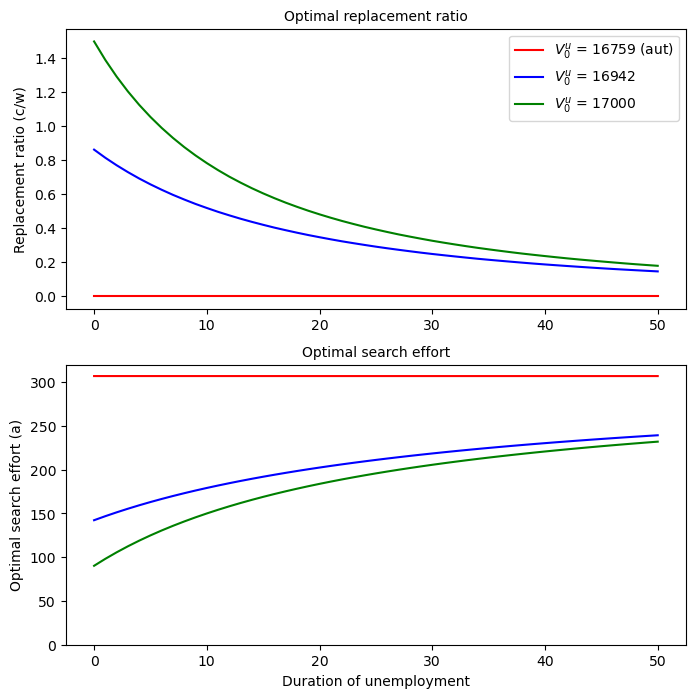

40.4.1. Replacement Ratios and Continuation Values#

Let’s graph the replacement ratio (

We’ll do this for three levels of

We accomplish this by using the optimal policy functions V_star, cons_star and a_star computed above as well the following iterative procedure:

# Replacement ratio and effort as a function of unemployment duration

T_max = 52

Vu_t = np.empty((T_max,3))

cons_t = np.empty((T_max-1,3))

a_t = np.empty((T_max-1,3))

# Calculate the replacement ratios depending on different initial

# promised values

Vu_0_hold = np.array([Vu_aut,16942,17000])

for i,Vu_0, in enumerate(Vu_0_hold):

Vu_t[0,i] = Vu_0

for t in range(1,T_max):

cons_t[t-1,i] = cons_star_interp(Vu_t[t-1,i])

a_t[t-1,i] = a_star_interp(Vu_t[t-1,i])

Vu_t[t,i] = V_star_interp(Vu_t[t-1,i])

fontSize = 10

plt.rc('font', size=fontSize) # controls default text sizes

plt.rc('axes', titlesize=fontSize) # fontsize of the axes title

plt.rc('axes', labelsize=fontSize) # fontsize of the x and y labels

plt.rc('xtick', labelsize=fontSize) # fontsize of the tick labels

plt.rc('ytick', labelsize=fontSize) # fontsize of the tick labels

plt.rc('legend', fontsize=fontSize) # legend fontsize

f1 = plt.figure(figsize = (8,8))

plt.subplot(2,1,1)

plt.plot(range(T_max-1),cons_t[:,0]/params.w,label = '$V^u_0$ = 16759 (aut)',color = 'red')

plt.plot(range(T_max-1),cons_t[:,1]/params.w,label = '$V^u_0$ = 16942',color = 'blue')

plt.plot(range(T_max-1),cons_t[:,2]/params.w,label = '$V^u_0$ = 17000',color = 'green')

plt.ylabel("Replacement ratio (c/w)")

plt.legend()

plt.title("Optimal replacement ratio")

plt.subplot(2,1,2)

plt.plot(range(T_max-1),a_t[:,0],color = 'red')

plt.plot(range(T_max-1),a_t[:,1],color = 'blue')

plt.plot(range(T_max-1),a_t[:,2],color = 'green')

plt.ylim(0,320)

plt.ylabel("Optimal search effort (a)")

plt.xlabel("Duration of unemployment")

plt.title("Optimal search effort")

plt.show()

For an initial promised value

But for

40.4.2. Interpretations#

The downward slope of the replacement ratio when

By providing the worker with a duration-dependent schedule of replacement ratios, the planner induces the worker in effect to reveal his/her search effort to the planner.

We saw earlier that with full information, the planner would smooth consumption over an unemployment spell by keeping the replacement ratio constant.

With private information, the planner can’t observe the worker’s search effort and therefore makes the replacement ratio fall.

Evidently, search effort rise as the duration of unemployment increases, especially early in an unemployment spell.

There is a carrot-and-stick aspect to the replacement rate and search effort schedules:

the carrot occurs in the forms of high compensation and low search effort early in an unemployment spell.

the stick occurs in the low compensation and high effort later in the spell.

We shall encounter a related carrot-and-stick feature in our other lectures about dynamic programming squared.

The planner offers declining benefits and induces increased search effort as the duration of an unemployment spell rises in order to provide an unemployed worker with proper incentives, not to punish an unlucky worker who has been unemployed for a long time.

The planner believes that a worker who has been unemployed a long time is unlucky, not that he has done anything wrong (e.g.,that he has not lived up to the contract).

Indeed, the contract is designed to induce the unemployed workers to search in the way the planner expects.

The falling consumption and rising search effort of the unlucky ones with long unemployment spells are simply costs that have to be paid in order to provide proper incentives.